Fit a multivariate linear model by robust regression using a simple M estimator that down-weights observations with large residuals

Fitting is done by iterated re-weighted least squares (IWLS), using weights

based on the Mahalanobis squared distances of the current residuals from the

origin, and a scaling (covariance) matrix calculated by

cov.trob. The design of these methods were loosely

modeled on rlm.

These S3 methods are designed to provide a specification of a class of

robust methods which extend mlms, and are therefore compatible with

other mlm extensions, including Anova and

heplot.

An internal vcov.mlm function is an extension of the standard

vcov method providing for the use of observation weights.

A plot.robmlm method provides simple index plots of case weights

to visualize those that were down-weighted.

Usage

robmlm(X, ...)

# Default S3 method

robmlm(

X,

Y,

w,

P = 2 * pnorm(4.685, lower.tail = FALSE),

tune,

max.iter = 100,

psi = psi.bisquare,

tol = 1e-06,

initialize,

verbose = FALSE,

...

)

# S3 method for class 'formula'

robmlm(

formula,

data,

subset,

weights,

na.action,

model = TRUE,

contrasts = NULL,

...

)

# S3 method for class 'robmlm'

print(x, ...)

# S3 method for class 'robmlm'

summary(object, ...)

# S3 method for class 'summary.robmlm'

print(x, ...)Arguments

- X

for the default method, a model matrix, including the constant (if present)

- ...

other arguments, passed down. In particular relevant control arguments can be passed to the to the

robmlm.defaultmethod.- Y

for the default method, a response matrix

- w

prior observation weights

- P

two-tail probability, to find cutoff quantile for chisq (tuning constant); default is set for bisquare weight function

- tune

tuning constant (if given directly)

- max.iter

maximum number of iterations

- psi

robustness weight function;

psi.bisquareis the default- tol

convergence tolerance, maximum relative change in coefficients

- initialize

modeling function to find start values for coefficients, equation-by-equation; if absent WLS (

lm.wfit) is used- verbose

show iteration history? (

TRUEorFALSE)- formula

a formula of the form

cbind(y1, y2, ...) ~ x1 + x2 + ....- data

a data frame from which variables specified in

formulaare preferentially to be taken.- subset

An index vector specifying the cases to be used in fitting.

- weights

a vector of prior weights for each case.

- na.action

A function to specify the action to be taken if

NAs are found. The 'factory-fresh' default action in R isna.omit, and can be changed byoptions(na.action=).- model

should the model frame be returned in the object?

- contrasts

optional contrast specifications; see

lmfor details.- x

a

robmlmobject- object

a

robmlmobject

Value

An object of class "robmlm" inheriting from c("mlm", "lm").

This means that the returned "robmlm" contains all the components of

"mlm" objects described for lm, plus the

following:

- weights

final observation weights

- iterations

number of iterations

- converged

logical: did the IWLS process converge?

The generic accessor functions coefficients,

effects, fitted.values and

residuals extract various useful features of the value

returned by robmlm.

Details

Weighted least squares provides a method for correcting a variety of problems in linear models by estimating parameters that minimize the weighted sum of squares of residuals \(\Sigma w_i e_i^2\) for specified weights \(w_i, i = 1, 2, \dots n\).

M-estimation generalizes this by minimizing the sum of a symmetric function \(\rho(e_i)\) of the residuals, where the function is designed to reduce the influence of outliers or badly fit observations. The function \(\rho(e_i) = | e_i |\) minimizes the least absolute values, while the bisquare function uses an upper bound on influence. For multivariate problems, a simple method is to use Mahalanobis \(D^2 (\mathbf{e}_i)\) to calculate the weights.

Because the weights and the estimated coefficients depend on each other, this is done iteratively, computing weights and then re-estimating the model with those weights until convergence.

References

A. Marazzi (1993) Algorithms, Routines and S Functions for Robust Statistics. Wadsworth & Brooks/Cole.

See also

plot.robmlm for a plot method;

rlm, cov.trob

Other robust methods:

Mahalanobis(),

plot.robmlm()

Examples

# Skulls data

# -----------

data(Skulls)

# make shorter labels for epochs and nicer variable labels in heplots

Skulls$epoch <- factor(Skulls$epoch, labels=sub("c","",levels(Skulls$epoch)))

# variable labels

vlab <- c("maxBreadth", "basibHeight", "basialLength", "nasalHeight")

# fit manova model, classically and robustly

sk.mod <- lm(cbind(mb, bh, bl, nh) ~ epoch, data=Skulls)

sk.rmod <- robmlm(cbind(mb, bh, bl, nh) ~ epoch, data=Skulls)

# standard mlm methods apply here

coefficients(sk.rmod)

#> mb bh bl nh

#> (Intercept) 133.9539529 132.6656599 96.50561801 50.8900600

#> epoch.L 4.1659721 -2.1793681 -4.84240950 1.1168866

#> epoch.Q -0.3671411 -1.3069085 -0.04276618 0.2817763

#> epoch.C -0.5833713 -0.7912067 1.03002114 -0.8379419

#> epoch^4 0.6350148 0.8787857 -0.55919989 -0.6233314

# index plot of weights

plot(sk.rmod, segments = TRUE, col = Skulls$epoch)

points(sk.rmod$weights, pch=16, col=Skulls$epoch)

text(x = 15+seq(0,120,30), y = 1.05, labels=levels(Skulls$epoch), xpd=TRUE)

# heplots to see effect of robmlm vs. mlm

heplot(sk.mod, hypotheses=list(Lin="epoch.L", Quad="epoch.Q"),

xlab=vlab[1], ylab=vlab[2], cex=1.25, lty=1)

heplot(sk.rmod, hypotheses=list(Lin="epoch.L", Quad="epoch.Q"),

add=TRUE, error.ellipse=TRUE, lwd=c(2,2), lty=c(2,2),

term.labels=FALSE, hyp.labels=FALSE, err.label="")

# heplots to see effect of robmlm vs. mlm

heplot(sk.mod, hypotheses=list(Lin="epoch.L", Quad="epoch.Q"),

xlab=vlab[1], ylab=vlab[2], cex=1.25, lty=1)

heplot(sk.rmod, hypotheses=list(Lin="epoch.L", Quad="epoch.Q"),

add=TRUE, error.ellipse=TRUE, lwd=c(2,2), lty=c(2,2),

term.labels=FALSE, hyp.labels=FALSE, err.label="")

##############

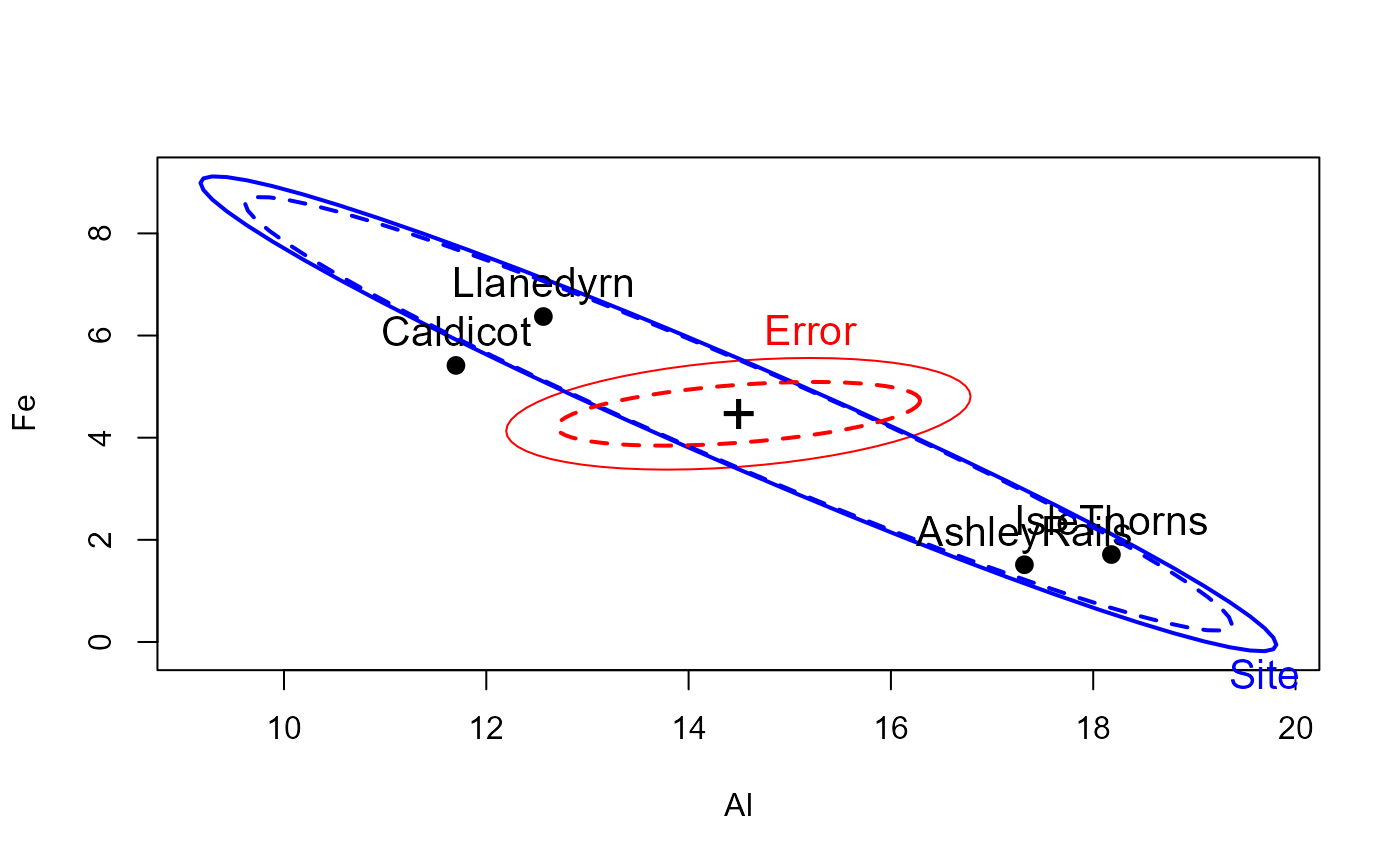

# Pottery data

data(Pottery, package = "carData")

pottery.mod <- lm(cbind(Al,Fe,Mg,Ca,Na)~Site, data=Pottery)

pottery.rmod <- robmlm(cbind(Al,Fe,Mg,Ca,Na)~Site, data=Pottery)

car::Anova(pottery.mod)

#>

#> Type II MANOVA Tests: Pillai test statistic

#> Df test stat approx F num Df den Df Pr(>F)

#> Site 3 1.5539 4.2984 15 60 2.413e-05 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

car::Anova(pottery.rmod)

#>

#> Type II MANOVA Tests: Pillai test statistic

#> Df test stat approx F num Df den Df Pr(>F)

#> Site 3 1.975 6.5516 15 51 1.722e-07 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

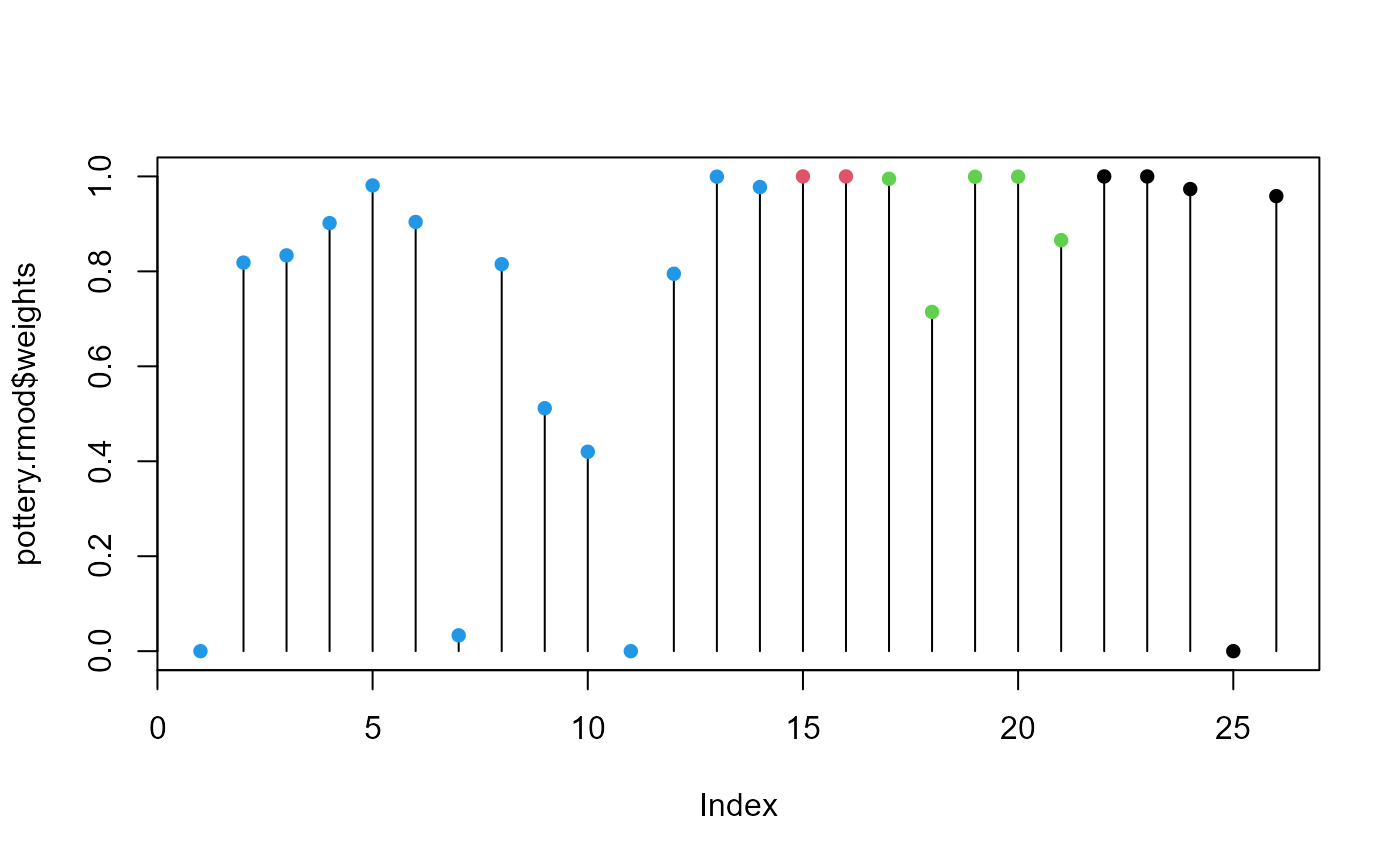

# index plot of weights

plot(pottery.rmod$weights, type="h")

points(pottery.rmod$weights, pch=16, col=Pottery$Site)

##############

# Pottery data

data(Pottery, package = "carData")

pottery.mod <- lm(cbind(Al,Fe,Mg,Ca,Na)~Site, data=Pottery)

pottery.rmod <- robmlm(cbind(Al,Fe,Mg,Ca,Na)~Site, data=Pottery)

car::Anova(pottery.mod)

#>

#> Type II MANOVA Tests: Pillai test statistic

#> Df test stat approx F num Df den Df Pr(>F)

#> Site 3 1.5539 4.2984 15 60 2.413e-05 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

car::Anova(pottery.rmod)

#>

#> Type II MANOVA Tests: Pillai test statistic

#> Df test stat approx F num Df den Df Pr(>F)

#> Site 3 1.975 6.5516 15 51 1.722e-07 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

# index plot of weights

plot(pottery.rmod$weights, type="h")

points(pottery.rmod$weights, pch=16, col=Pottery$Site)

# heplots to see effect of robmlm vs. mlm

heplot(pottery.mod, cex=1.3, lty=1)

heplot(pottery.rmod, add=TRUE, error.ellipse=TRUE, lwd=c(2,2), lty=c(2,2),

term.labels=FALSE, err.label="")

# heplots to see effect of robmlm vs. mlm

heplot(pottery.mod, cex=1.3, lty=1)

heplot(pottery.rmod, add=TRUE, error.ellipse=TRUE, lwd=c(2,2), lty=c(2,2),

term.labels=FALSE, err.label="")

###############

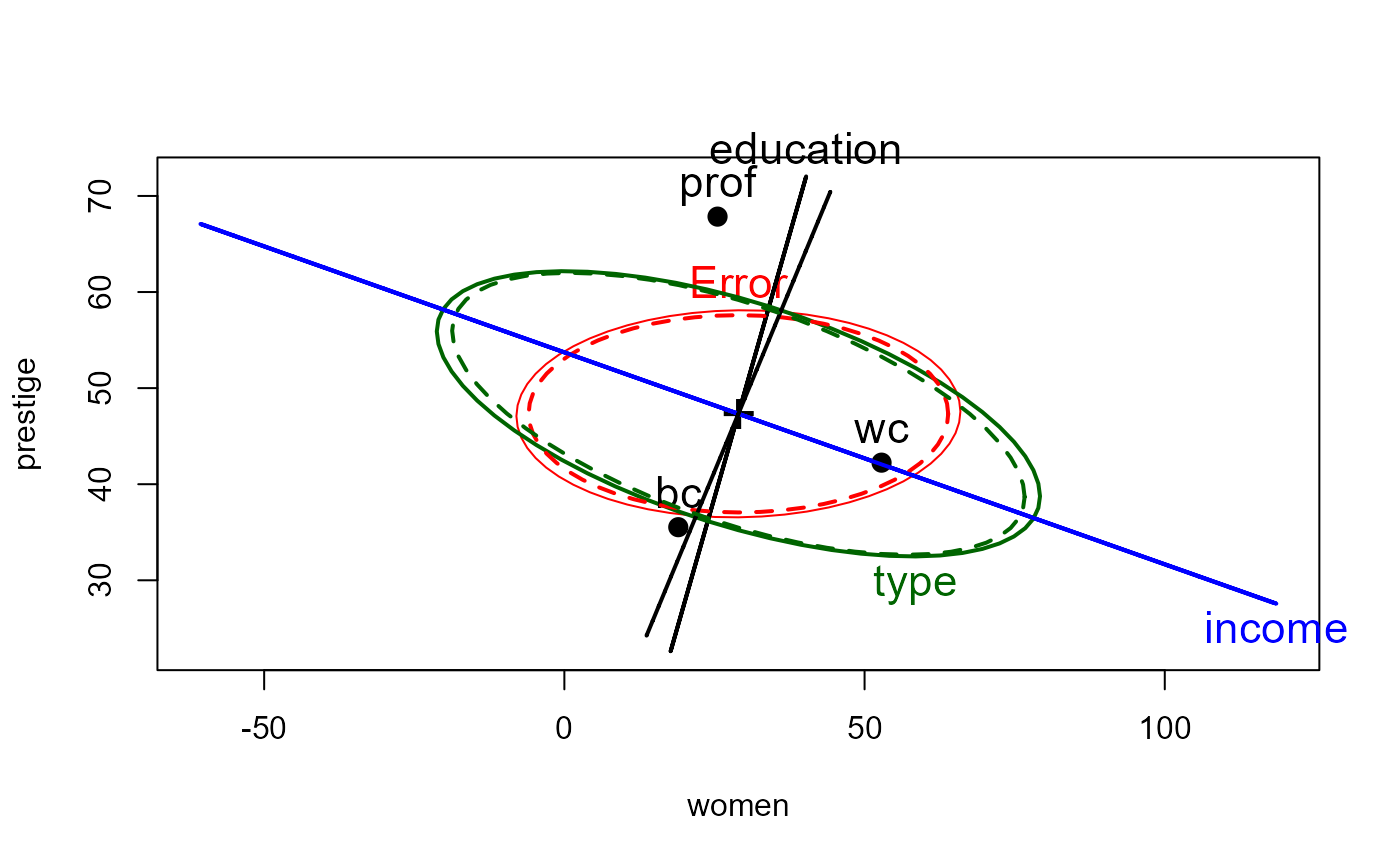

# Prestige data

data(Prestige, package = "carData")

# treat women and prestige as response variables for this example

prestige.mod <- lm(cbind(women, prestige) ~ income + education + type, data=Prestige)

prestige.rmod <- robmlm(cbind(women, prestige) ~ income + education + type, data=Prestige)

coef(prestige.mod)

#> women prestige

#> (Intercept) 29.638865042 -0.622929165

#> income -0.004594789 0.001013193

#> education 1.677749298 3.673166052

#> typeprof 20.761455686 6.038970651

#> typewc 27.911084356 -2.737230718

coef(prestige.rmod)

#> women prestige

#> (Intercept) 24.696906731 0.019651597

#> income -0.004902077 0.001082214

#> education 2.352283991 3.549614674

#> typeprof 18.737098949 6.394466644

#> typewc 26.762870920 -2.570933052

# how much do coefficients change?

round(coef(prestige.mod) - coef(prestige.rmod),3)

#> women prestige

#> (Intercept) 4.942 -0.643

#> income 0.000 0.000

#> education -0.675 0.124

#> typeprof 2.024 -0.355

#> typewc 1.148 -0.166

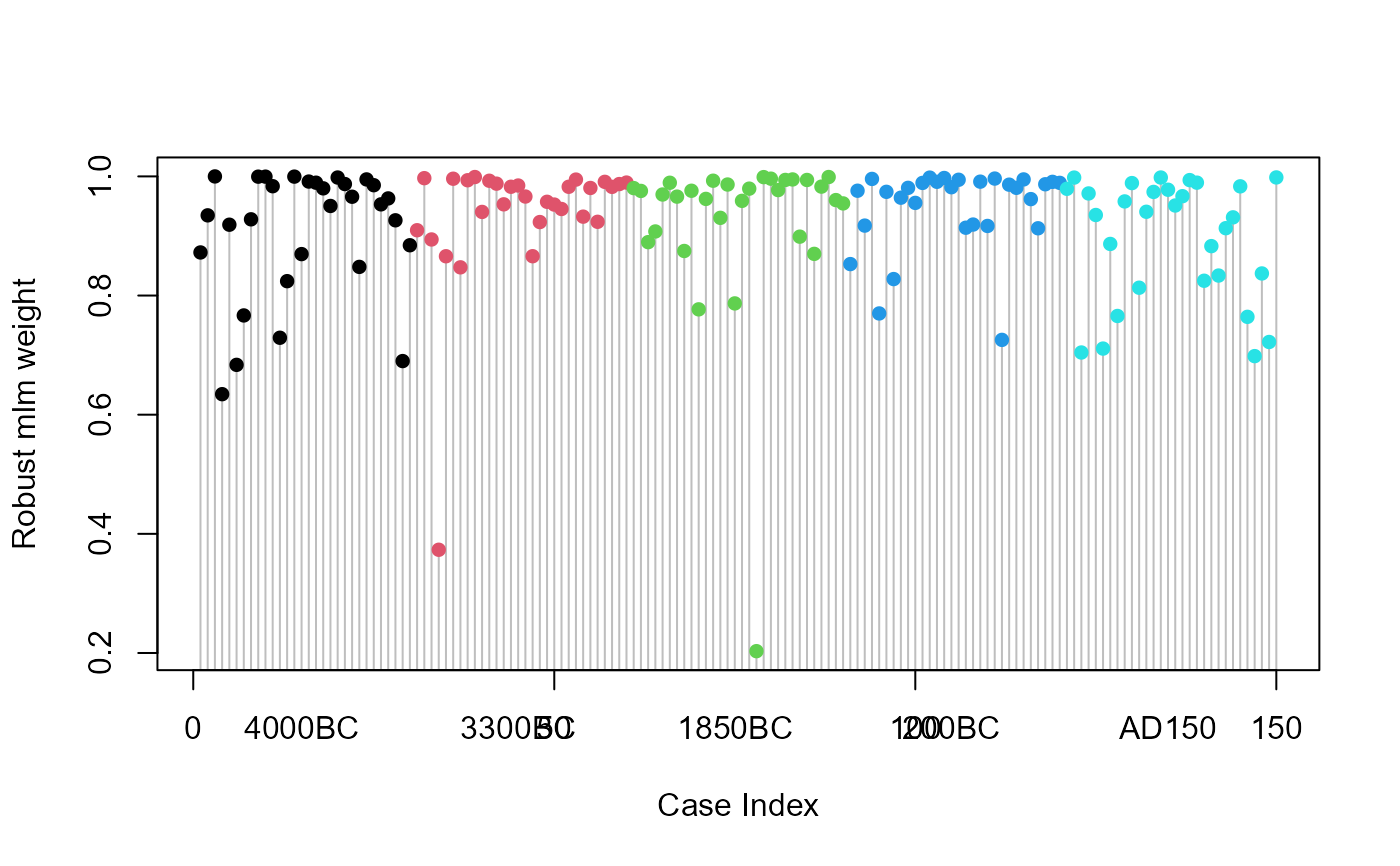

# pretty plot of case weights

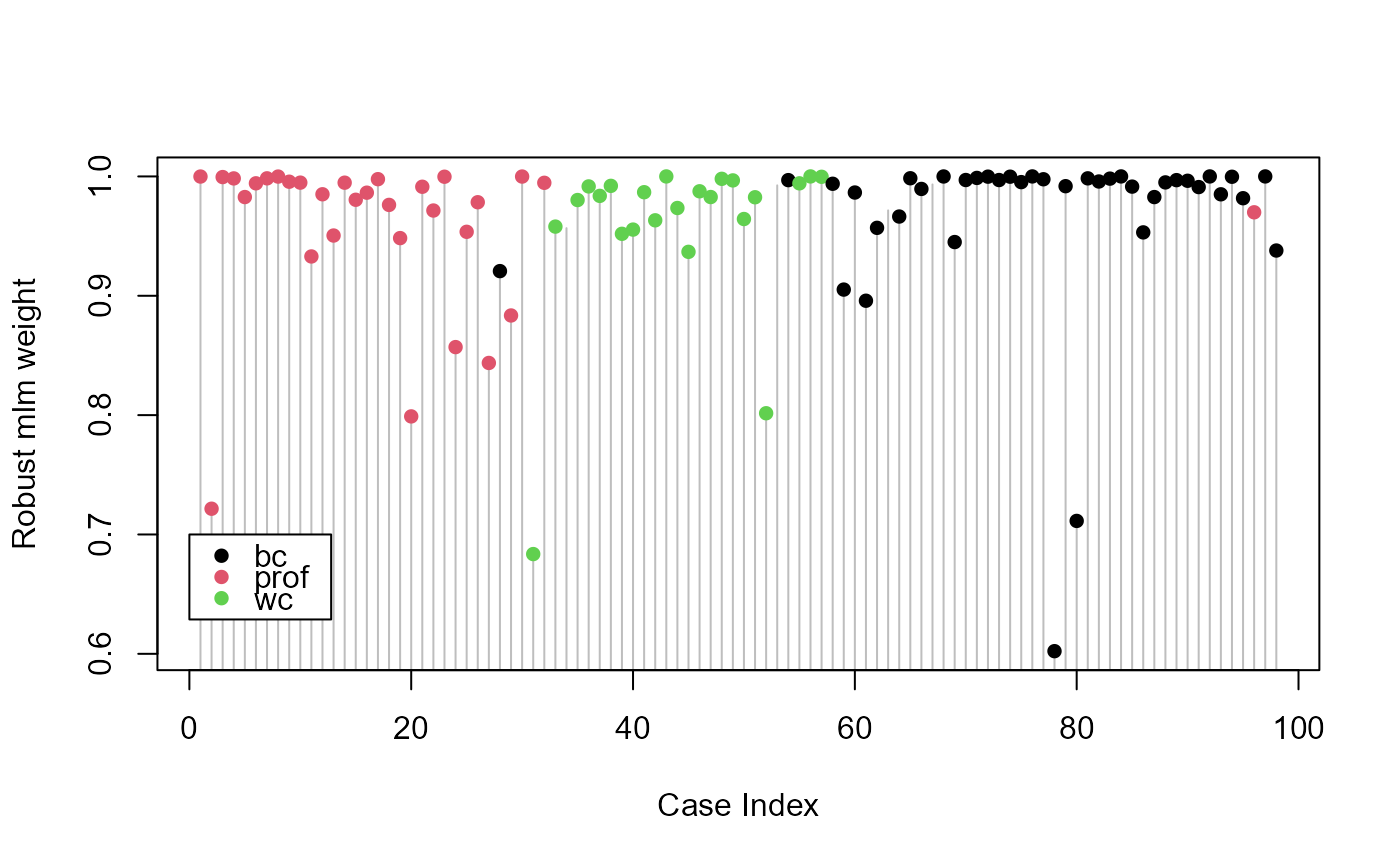

plot(prestige.rmod$weights, type="h", xlab="Case Index", ylab="Robust mlm weight", col="gray")

points(prestige.rmod$weights, pch=16, col=Prestige$type)

legend(0, 0.7, levels(Prestige$type), pch=16, col=palette()[1:3], bg="white")

###############

# Prestige data

data(Prestige, package = "carData")

# treat women and prestige as response variables for this example

prestige.mod <- lm(cbind(women, prestige) ~ income + education + type, data=Prestige)

prestige.rmod <- robmlm(cbind(women, prestige) ~ income + education + type, data=Prestige)

coef(prestige.mod)

#> women prestige

#> (Intercept) 29.638865042 -0.622929165

#> income -0.004594789 0.001013193

#> education 1.677749298 3.673166052

#> typeprof 20.761455686 6.038970651

#> typewc 27.911084356 -2.737230718

coef(prestige.rmod)

#> women prestige

#> (Intercept) 24.696906731 0.019651597

#> income -0.004902077 0.001082214

#> education 2.352283991 3.549614674

#> typeprof 18.737098949 6.394466644

#> typewc 26.762870920 -2.570933052

# how much do coefficients change?

round(coef(prestige.mod) - coef(prestige.rmod),3)

#> women prestige

#> (Intercept) 4.942 -0.643

#> income 0.000 0.000

#> education -0.675 0.124

#> typeprof 2.024 -0.355

#> typewc 1.148 -0.166

# pretty plot of case weights

plot(prestige.rmod$weights, type="h", xlab="Case Index", ylab="Robust mlm weight", col="gray")

points(prestige.rmod$weights, pch=16, col=Prestige$type)

legend(0, 0.7, levels(Prestige$type), pch=16, col=palette()[1:3], bg="white")

heplot(prestige.mod, cex=1.4, lty=1)

heplot(prestige.rmod, add=TRUE, error.ellipse=TRUE, lwd=c(2,2), lty=c(2,2),

term.labels=FALSE, err.label="")

heplot(prestige.mod, cex=1.4, lty=1)

heplot(prestige.rmod, add=TRUE, error.ellipse=TRUE, lwd=c(2,2), lty=c(2,2),

term.labels=FALSE, err.label="")